CRA’s Energy Practice regularly monitors FERC regulatory accounting audit activity to ensure our clients are up to date on compliance trends and are prepared to successfully meet FERC audit requirements.

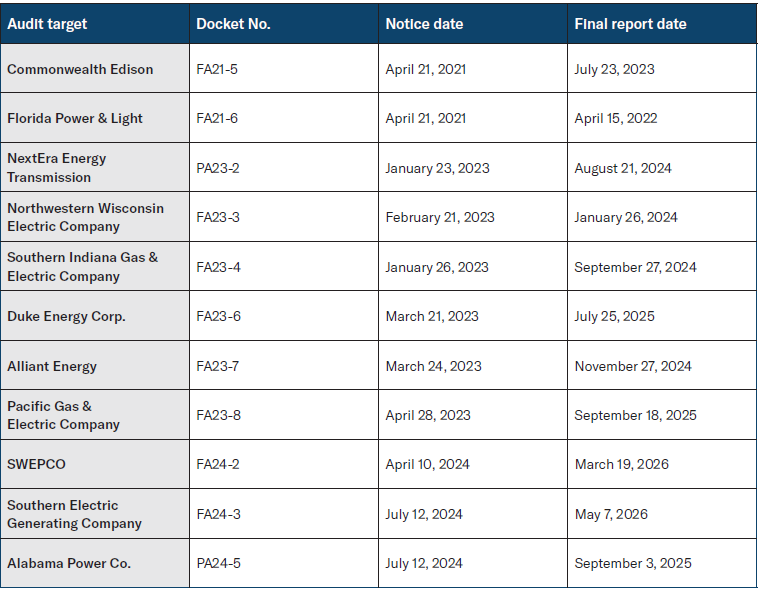

We recently reviewed Final Audit Reports issued between April 2022 and May 2026 (See Table 1) by the FERC’s Division of Audits and Accounting (DAA), part of FERC’s Office of Enforcement and Regulatory Accounting (OERA). The scope of these audits includes accounting regulations in 18 C.F.R. Part 101, which contains FERC accounting regulations as maintained under its Uniform System of Accounts.

These audits focus on regulatory accounting primarily for formula electric transmission ratesetting. We compared these results with those of our initial review on this audit scope between 2018 and 2021.

Table 1: Regulatory accounting FERC audits 2022-2026

Current FERC audit pace is steady and robust and consistent with prior periods, with about 10 open audits at any time.

What did we find?

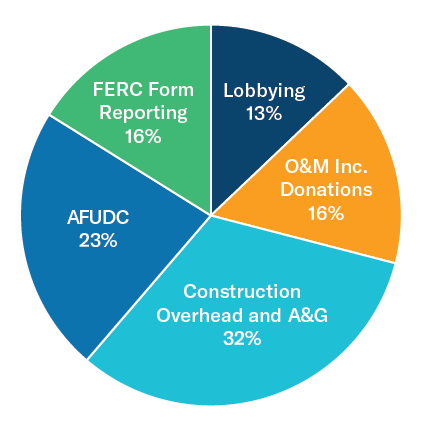

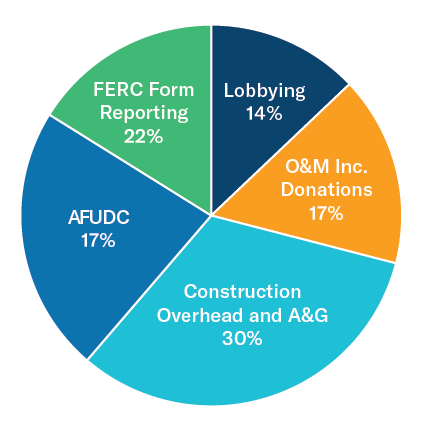

The charts below compare regulatory accounting findings along broad categories as shown between 2018-2021 and 2022-2026, as observed by CRA.

Common FERC audit issues 2018-2021

Common FERC audit issues 2022-2026

CRA observes the following:

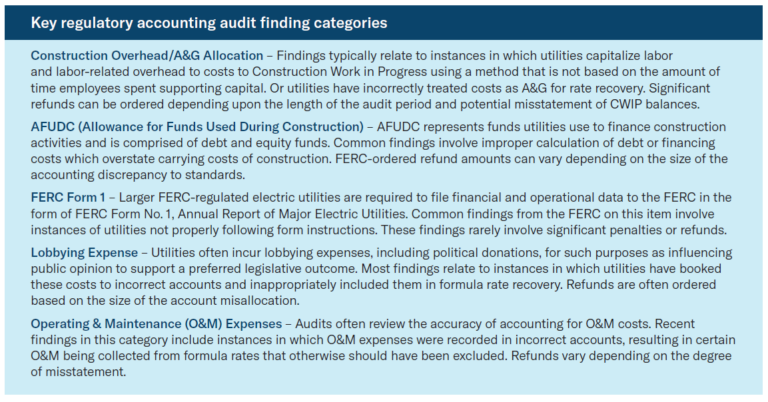

- Common regulatory accounting findings1 fell into 5 key categories:

a. Construction Overhead and A&G Treatment

b. Allowance for Funds Used During Construction (AFUDC)

c. FERC Form 1 Reporting

d. Lobbying Expenses; and

e. Operation & Maintenance Expenses (O&M)

(See the table at the bottom of this article for category definitions) - These key categories have not changed significantly from those we observed in our 2018-2021 review of DAA audits and represent the current areas for audit results.

- Construction Overhead and A&G Treatment holds the largest share, with nearly 1/3 of common findings associated with it. This category is also associated with the largest penalties and settlements (as much as $70 million plant write-down2).

- Calculation of AFUDC and FERC Form 1 Reporting continue to be prominent categories of findings after Construction Overhead and A&G Treatment.

What does this mean for FERC-regulated utilities?

Recent audit activity indicates that the FERC has maintained a consistent audit pace for regulatory compliance in recent years, with about 10 audits open at any time.

Will your utility be next? All FERC-regulated utilities are subject to a FERC DAA regulatory accounting audit – especially larger electric transmission-owning companies, although small to mid-sized companies can also be an audit target.

The topic of overhead labor to construction continues to be a focus for FERC. As part of their compliance planning, utilities should review their current regulatory accounting policy for overhead labor costs to construction and evaluate whether they meet the FERC’s standards articulated through these recent audit results. Companies that demonstrate a regulatory accounting policy that allocates labor costs to construction based on a definitive relationship to employee time will be positioned to sustain an audit and avoid financial consequences.

Keep abreast of FERC DAA audit activity and look for CRA’s next publication, which will explore specific steps utilities can take now to prepare for a FERC regulatory accounting audit.

1 Findings in category occurring 5 or more times across the audit pool full set of findings.

2 Commonwealth Edison Company, Docket Nos. FA21-5-000, FA21-5-001, Submission of Settlement Agreement and Motion Requesting Expedited Action, February 11, 2025.