Rising pharmaceutical expenditure is impacting France’s healthcare budget.

Expenditure on reimbursed health products continues to rise in France, with total spending on reimbursed medicines reaching €37.2 billion in 2024, representing a 6.7% increase compared to 2023. In parallel, spending on reimbursed medical devices and procedures climbed to €11.6 billion, an increase of 5.4%. Hospital spending also showed significant structural pressure, with “liste en sus” medicines rising to €7.7 billion in 2024, an increase of 14.4% from 2023.1

Key takeaways

This article focuses on the following points:

- The French Social Security Financing Act 2026 avoids the most aggressive proposals but still targets record savings of €2.3 billion from medicines and health products.

- Rebates are the primary cost containment tool, with a small number of high-cost medicines driving a large share of paybacks.

- LFSS 2026 accelerates cost containment by normalising biosimilars, while simultaneously supporting innovation through a permanent direct market access pathway that shortens reimbursement time for eligible medicines under provisional pricing.

- The reformed safeguard clause will materially affect industry economics, shifting payback calculations to reimbursed spending and increasing repayment levels if national drug spending exceeds set thresholds.

As these rising levels of pharmaceutical expenditure place increasing pressure on the healthcare budget, an important part of the adjustment is occurring through the growing weight of rebates applied to reimbursed medicines (>10% increase in total rebates from 2023 to 2024).

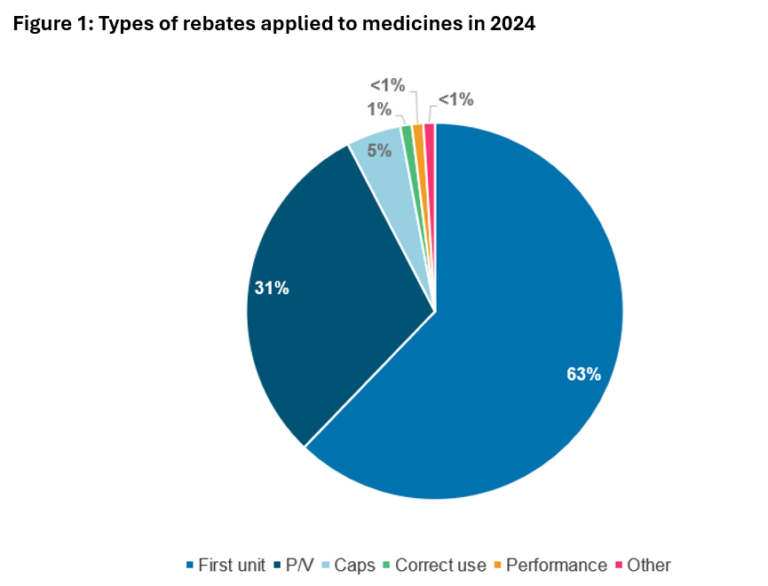

In 2024, rebate mechanisms were applied to almost 400 products, with half of all rebate amounts coming from only 14 products. ~65% of rebates were triggered from the very first unit sold. ~30% were based on price/volume (P/V) agreements. The rest were related to caps or other metrics (Figure 1).1

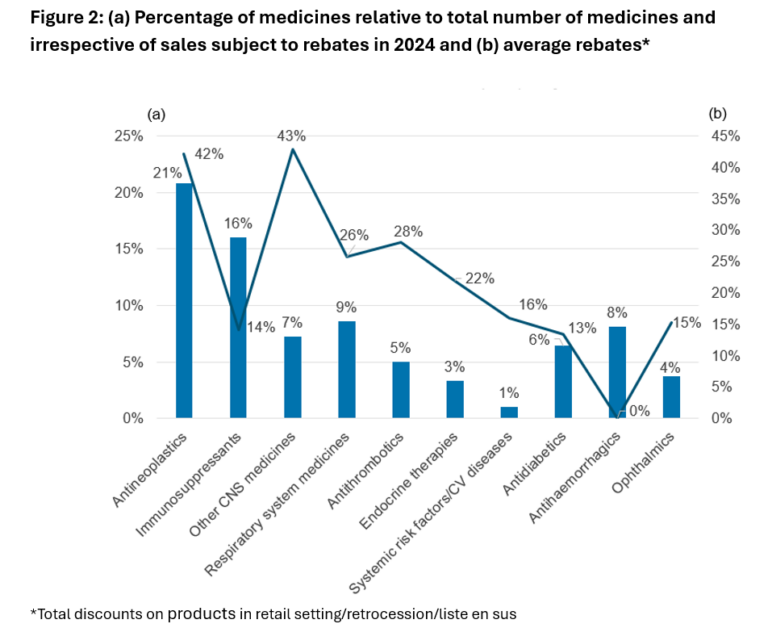

Therapeutic areas were not equally subject to discounts. The highest rates of discounts were observed in oncology and central nervous system medicines (>40% on average); while <10% of most medicines were subject to discounts, 15%–20% of immunosuppressants and antineoplastic agents were subject to discounts (Figure 2).1

Key measures of the French Social Security Financing Act (LFSS) 2026

Containing costs without overly aggressive measures

Heated debates occurred in the French political arena over the introduction of aggressive cost containment measures. Tough options were proposed during the legislative process, including mandatory discounts on Amélioration du Service Médical Rendu (ASMR) IV-V products and delisting of Service Médical Rendu (SMR) low products.2 These measures were dropped in the 2026 social security financing law, Loi de Financement de la Sécurité Sociale (LFSS), promulgated on December 31, 2025.3

By stepping back from these proposals, the law signals a less aggressive stance on cost containment for patented medicines, but still aims to restore balance in public spending by generating record‑level savings of €2.3 billion on medicines and health products.4

Strengthening support for community pharmacies

One of the key elements of the LFSS 2026 is focused on strengthening the regulation and support of community pharmacies. The law formalises ceilings for generic and biosimilar rebates – 40% and 20% respectively – securing revenue streams for pharmacies and protecting them from future regulatory changes. Additionally, conventional aid for pharmacies in difficulty is extended beyond fragile territories, a change expected to benefit around 800 additional pharmacies. Finally, pharmacists are now authorised to manage specific clinical situations with appropriate remuneration. These measures extend operational and financial support to the sector while recognising the ongoing pressures faced by pharmacies.4

Faster market access to support innovation

Another key development in the LFSS 2026 is the permanent establishment of the direct market access scheme, showing efforts to continue supporting access to innovation. Introduced as a pilot in 2022, the scheme is designed to reduce delays between clinical assessment and reimbursement. Following a favourable opinion from the Haute Autorité de Santé (HAS), and a decision by the Ministry of Health, eligible medicines may receive temporary reimbursement for up to 12 months.

Eligibility is limited to medicines with an important or major SMR and an ASMR I-IV. Where no price has been set for the indication, manufacturers may apply a provisional price during this period, subject to statutory rebates, before transitioning to a standard reimbursement using a price agreed upon by the Comité économique des produits de santé (CEPS).9 So far, only five medicines have entered the scheme, including one which exited the program following unsuccessful price negotiations.10 But for those that achieved reimbursement, the time from EMA approval to access was twice as quick as under standard procedures.5 CRA is currently undertaking a detailed review of the scheme’s early performance, with further insights to follow.

Pharmaceutical expenditure control through biosimilars acceleration

Despite these measures, the law does not lose sight of its overall expenditure control objectives, with pharmaceutical companies expected to contribute €1.4 billion through price reductions, including €0.2 billion each on generics and medical devices.2 These reductions are not treated in isolation, but are closely linked to a broader push to use medicines more efficiently.

One of the most visible levers in this respect is the acceleration of biosimilar uptake. A tightening of prescription, dispensing, and reimbursement rules that progressively align biosimilars with the generic framework supports this initiative. Third-party payment for biosimilars, prescribing by international non-proprietary name (INN), and tighter restrictions on the “non‑substitutable” designation place biosimilars firmly within the framework already applied to generics.4

In practice, substitution by the pharmacist is permitted only within officially defined groups of biologically similar medicines; prescribers may oppose this substitution solely through an explicit, medically justified mention on the prescription. These rules are accompanied by requirements to ensure the traceability of biological medicines, notably through brand‑name identification.8 The objective is not only to reduce costs, but also to normalise biosimilars as routine therapeutic options across care pathways.

Reform of the safeguard clause

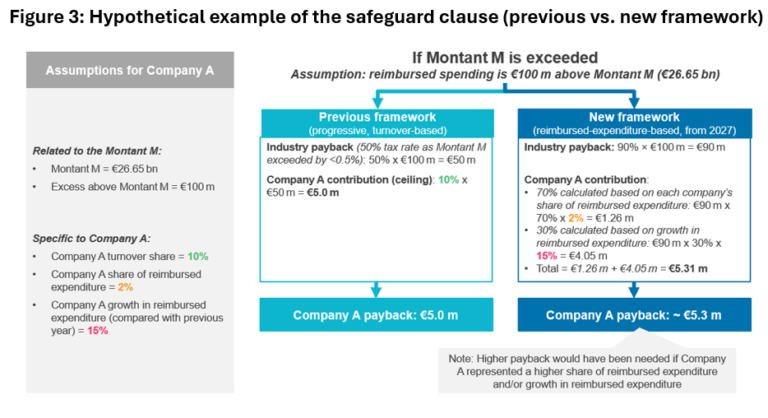

The law also introduces a structural reform that will shape pharmaceutical spending in the years ahead, the overhaul of the safeguard clause, with application from the 1st of January 2027. Historically, this mechanism triggered industry payback when social security spending exceeded a threshold calculated from company turnover. Recent changes have been made to the basis and the logic of the system, with the aim of making pharmaceutical contributions to health spending more predictable and transparent.

The clause is now based on reimbursed expenditure in France rather than company turnover, with the annual threshold, Montant M, set at €26.65 billion for 2026.6 Montant M is determined each year in the LFSS based on forecasts of reimbursed drug spending, rather than through a fixed formula. Reimbursed medicines apart from generics and biosimilars are considered, as well as products granted early access or direct access, and those subject to AMM Miroir rebates.† If total reimbursed spending exceeds Montant M, companies will repay 90% of the amount spent above the threshold,6 replacing the previous progressive payback system of 50%–70% depending on the amount exceeded.7

Contributions are now calculated based on two metrics. 70% of contributions are calculated based on each company’s share of reimbursed expenditure, and 30% are based on the growth of that expenditure compared with the previous year, with a 12% cap on each company’s reimbursed expenditure limiting individual exposure.6 An example of the impact on companies is provided in Figure 3. By shifting from turnover to reimbursed spending and establishing a clear threshold, the system provides greater predictability for the industry, but could be associated with greater amounts to be paid back by companies.

Who feels the impact…and what comes next?

While some European markets, such as the UK, have taken steps to adjust ICER thresholds as a consequence of the US Most Favoured Nation (MFN) order, the LFSS 2026 does not signal any movement toward an MFN-type convergence, reflecting a national effort to reinforce cost containment.

Indeed, while access to innovation may be supported with the direct market access scheme, tighter control of drug spending is expected through stronger volume steering towards biosimilar uptake and a more predictable and structured financial correction mechanism with the safeguard clause.

This evolving environment is expected to weigh most heavily on manufacturers of generics and biosimilars, but questions around the impact on ASMR IV–V products and high-cost combination therapies remain, given the €1.4 billion savings expected to be achieved by price reduction.6 As a result, 2026 is shaping up to be a decisive year for market access and pricing strategy in France, with policymakers walking a fine line between sustaining industrial incentives and enforcing budget discipline.

Whether the system succeeds in striking the right balance between supporting innovation and maintaining affordability will only become clear at the end of the year, but the choices made in 2026 are likely to have lasting consequences for both pricing strategy and the credibility of France’s innovation narrative.

†The AMM Miroir mechanism allows a drug without market authorization (MA) to be reimbursed when it is used in combination with another drug that does have MA for that specific combination. However, for the drug that lacks MA, reimbursement is only granted if mandatory rebates are applied.

Bibliography:

- https://sante.gouv.fr/IMG/pdf/ceps_ra2024_version_definitive_decembre_2025.pdf

- https://www.pharmaceutical-technology.com/analyst-comment/pharma-critical-french-drug-pricing-reforms-pending-ceps-report/

- https://www.securite-sociale.fr/la-secu-en-detail/loi-de-financement/annee-en-cours

- https://www.fspf.fr/le-plfss-definitivement-adopte-la-mobilisation-de-la-fspf-a-paye

- https://sante.gouv.fr/soins-et-maladies/medicaments/professionnels-de-sante/autorisation-de-mise-sur-le-marche/article/dispositif-d-acces-direct-pour-certains-produits-de-sante

- https://www.senat.fr/rap/l25-131-21/l25-131-21.html

- https://smart-pharma.com/wp-content/uploads/2025/01/Healthcare-Costs-Regulation-in-France-VF.pdf

- https://www.ameli.fr/medecin/exercice-liberal/regles-de-prescription-et-formalites/medicaments-et-dispositifs/medicaments-biosimilaires/regles-de-prescription-et-de-delivrance

- https://www.has-sante.fr/jcms/r_1500918/fr/acces-precoce-a-un-medicament

- https://www.ispor.org/heor-resources/presentations-database/presentation-cti/ispor-europe-2025/poster-session-1-2/accelerating-therapeutic-innovation-early-results-from-france-s-acc-s-direct-scheme